The US Solar Industry is the Latest Victim to Trump’s War on Clean Energy

By Tom Lewis, Federal Policy Manager for Manufacturing & Industrial Policy

Solar manufacturing in the United States is facing significant new headwinds driven by recent policy developments. This includes actions by the Trump administration to make permitting new solar projects more difficult, and passage of the so-called “One Big Beautiful Bill Act” (OBBBA)—a sweeping piece of legislation that repeals clean energy and manufacturing incentives that were driving clean technology investment across the nation. The United States was once the world leader in solar manufacturing, but because of domestic policy choices and international developments, it has steadily lost ground. According to the International Energy Agency (IEA), in 2021, China produced 74.7% of the world’s module capacity, 85.1% of cell capacity, and 96.8% of wafer capacity. After the Inflation Reduction Act increased support for clean technology manufacturing and deployment in 2022, the United States experienced a boom in new solar manufacturing capacity. The Solar Energy Industry Association (SEIA) estimates there has been $43.8 billion of new investment in solar manufacturing since the bill’s passage.

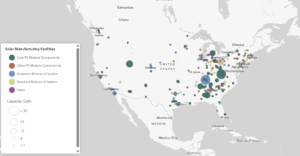

Click to access Solar Supply Chain map.

Investment in the manufacturing sector, particularly in strategic and next generation technologies such as solar, is critical for securing U.S. economic competitiveness. To assess the progress we’ve made to reshore the domestic solar supply chain and to understand the threats the sector faces because of these recent policy choices, the BlueGreen Alliance (BGA) conducted research to map and analyze domestic facilities within the full solar supply chain including core photovolactic (PV) module components, electronics, tracking and structural components, and additional parts that are required to produce a solar panel. We have identified 335 manufacturing facilities in the United States producing components for the solar supply chain, of which 264 are currently operational. Before federal manufacturing incentives were enacted, the United States had the capacity to produce 8 gigawatts (GW) of modules, but as of June 2025, the country now has the capacity to produce 57.5 GW of modules per year, which exceeds projected U.S. demand. Clearly, there has been progress to onshore the sector, but substantial investment is still required to develop a fully domestic supply chain.

Our analysis of the solar supply chain evaluates domestic manufacturing capacity using readily available data. We use the domestic supply rate as our primary metric for this evaluation because it can measure the degree to which domestic production fulfills domestic demand—indicating the overall strength of domestic manufacturing. We calculate the domestic supply rate by dividing total domestic capacity for each component by total domestic demand.

According to our research, while we have made a lot of progress expanding module production, the United States still has limited capacity to produce cells, and no capacity to produce ingots and wafers. This gap is unsurprising given the massive capital commitment required to set up new factories within the PV module supply chain. Firms are more likely to commit to onshoring the most downstream segment—modules—before they commit to the upstream of the supply chain. This dynamic is especially evident with cells, where the United States only recently onshored its first cell manufacturing facility since 2019. Additional cell manufacturing was expected to follow over the next half decade, driven by strong demand signals from the Inflation Reduction Act. Demand certainty is especially important for a capital-intensive industry, where it can take upwards of half a decade to bring a new facility online. This is why the Inflation Reduction Act provided both supply-push and demand-pull incentives to onshore the clean technology supply chain.

Unfortunately, the passage of the OBBBA introduced immense uncertainty for the sector. By repealing the solar deployment credit after 2027, and thereby ending the domestic content bonus, the law weakens the long-term demand signals for new solar manufacturing. For instance, because of OBBBA, Rhodium Group estimates that over the next decade, U.S. clean energy installations will be 57% to 65% lower than projections under the Inflation Reduction Act. Similarly, BloombergNEF (BNEF) projects a 41% decline in clean energy deployment after 2027. As a result, manufacturers will face downgraded growth estimates, while simultaneously losing the domestic content bonus that provided a strong incentive for developers to purchase their products.

For instance, because of OBBBA, Rhodium Group estimates that over the next decade, U.S. clean energy installations will be 57% to 65% lower than projections under the Inflation Reduction Act.

Additionally, the U.S. Environmental Protection Agency (EPA) recently announced it is planning to cut $7 billion in federal grants awarded through the “Solar for All” program. The program helped low- and moderate-income families install solar panels and expand community solar initiatives. It also served as an additional demand driver for domestically produced solar panels.

Repealing incentives is not the only tactic the Trump administration is using to target the solar industry. Trump continues to escalate his attacks on clean energy by making it harder to site projects. Trump’s executive order on “market distorting subsidies” for solar and wind is already impacting the financing of solar projects. Additionally, the Interior Department will now require previously routine reviews of solar projects to undergo additional political review through the secretary’s office. These actions are causing delays for projects both on public and private lands.

This is all occurring at a time when electricity demand is growing because of new manufacturing, data centers, and economy-wide electrification. The IEA expects electricity demand to increase 3.3% in 2025, a significant rise from earlier projections. All that load growth requires new energy generation, but the Trump administration is making it harder to deploy solar, the fastest growing and cheapest source of new power. The collapse in demand for new solar will also lead to new manufacturing investments being unviable and harm our ability to continue to onshore the supply chain. Indeed, since Trump took office factory cancellations in the solar supply chain have surged.

Companies that had signaled a commitment to invest billions in the United States to onshore our solar supply chain thanks to the demand certainty provided by the Inflation Reduction Act are now backtracking. These policies, along with other actions by the Trump administration, are starting to show themselves in the macro statistics. The Bureau of Labor Statistics reported that only 22,000 jobs were created in August, and revised data from June now shows a net loss of 13,000 jobs—the first time the nation has reported negative job growth since the height of the pandemic. For context, last year, the U.S. economy added an average of 168,000 jobs per month. The manufacturing sector has been particularly hard hit. All signs are unfortunately pointing to an economy-wide slump with a particular emphasis on our once booming solar industry.

Trump’s war on clean energy is sabotaging our economy, destroying jobs, and committing vulnerable communities around the country to a future of pollution.